Our Turkish Lira with its wounded convertibility

The economy management in Ankara may have this thought of stopping the devaluation of the Turkish Lira by wounding the lira’s convertibility but actually it also damages the debt capacity of the Treasury.

You will hold talks themed “Trade with national currencies” and at the same time you will wound the convertibility of the Turkish Lira; that seems incredible but it has happened. Turkish lira is rapidly losing in the last couple of years, the convertibility it obtained in the past quarter of a century by clawing its way up.

In order to prevent further devaluation of the lira, the Turkish Lira is banned to foreign institutions and banks, while at the same time foreign central banks are told “Here are Turkish Liras for you; give us the currency you have printed.” On the other hand, this is never asked, “Have I done whatever I need to do to protect my money other than banning my currency?”

No central bank whose currency is reserve currency wants to buy Turkish Lira and give their own money. Those that do so are not reserve currency anyway.

Ankara that is after swap lines from foreign central banks only cares about “balance sheet window dressing” and with the expression they love very much, “perception management.”

You have managed to provide yuan swap line and these yuans are recorded in the balance sheet. Well, can you sell these yuans and convert them to dollars in the international market? Probably not. Or can you convert the Qatari riyal? Even in London market, it might be hard to find the other party to convert 50 million riyals.

When the Turkish lira was banned to foreign institutions and banks, this has also annoyed the investments and investors that entered the country freely before. It has created a sale pressure on financial investments such as stocks and equities. As a matter of fact, as of the beginning of the year, portfolio investments that left the country have reached 10 billion dollars.

The economy management in Ankara may have this thought of stopping the devaluation of the Turkish Lira by wounding the lira’s convertibility but actually it also damages the debt capacity of the Treasury.

We understand that by almost nullifying the Turkish lira loan capacity of foreign institutions and banks as of the beginning of May, certain foreign institutions are increasingly having defaults in lira settlements.

As you know, the Banking Regulation and Supervision Agency (BDDK) on May 7 imposed a lira transaction ban on three foreign banks (BNP Paribas SA, Citibank NA, UBS AG) as they did not fulfill Turkish lira liabilities in due time. It then lifted this ban a couple of days later.

Actually, the conditions of this default situation were brought by the decisions made, with the ban on TL loaning.

After a week, on May 14, Europe’s two major international financial services, safekeeping and clearing institutions halted their Turkish Lira transactions. Clearstream and Euroclear institutions have jointly decided to suspend Turkish lira settlements (Delivery versus payment) over a shared electronic communications platform Bridge effective from May 18. They also noted that domestic settlements within their own system and internal settlements in lira would continue to operate as usual.

Obviously, these institutions have met with events of default due to investors who could not do their Turkish lira payments.

For this reason, in their statement they reminded that because overdraft credit lines were removed, they recommended that customers keep a buffer amount in their cash accounts in lira.

As a result, Ankara opted for a discourse and its accompanying action to change the perception in the eyes of the voter that the value loss of the Turkish lira was due to bad management. They spun it into the story of “foreign powers are attacking our economy.” This discourse and its accompanying actions have caused the current mechanisms to be disrupted in world markets and it pushed the Turkish lira into being a non-tradeable currency.

In the war of Ankara with “windmills,” the business has gone all the way to avoiding Turkish lira assets and even restricting the trade of Turkish lira assets.

On May 20, the BDDK announced it would exempt Euroclear Bank and Clearstream Banking from the lira ban. It actually wrote its mistake in its statement. This decision was to ensure the efficient trading of Turkish lira securities, and so the clearing operations of Turkish-lira-denominated bond and lease certificates transactions are not adversely affected, it said.

This means that they have not calculated any possible negative effects.

If you ask my opinion, the BDDK is still not aware of its mistake. They have not understood that Euroclear and Clearstream were not unable to find Turkish lira, but the investors, those who would have bought securities; in other words, investors who bought securities could not find Turkish lira and defaulted.

In another development, major banks which were pointed out to the public as “manipulators,” but were exempt from the transaction ban a couple of days later have decided to suspend their Turkish lira transactions.

Who is the loser here? It is us who want our currency to be widespread in the entire world and have a good commercial standing.

In a Bloomberg story on May 18, it said that BNP Paribas which was banned by BDDK on May 7 then later the ban was dropped, has decided to shrink its operations in the Turkish lira market. The bank’s foreign-exchange prime-brokerage unit has stopped offering customers new Turkish lira trades, the story said.

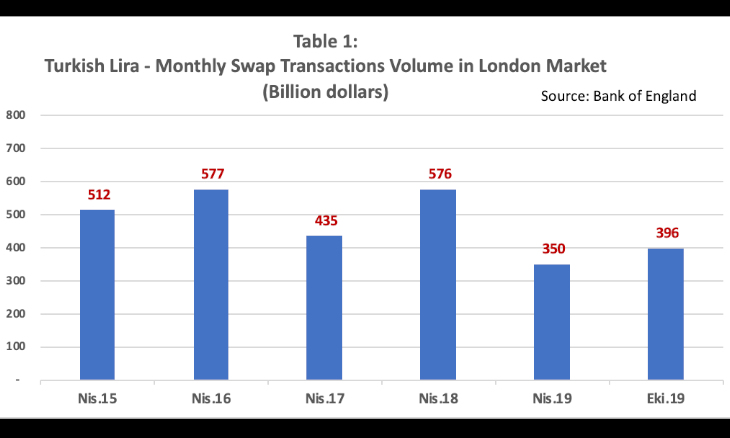

Until swap restrictions started in 2018, Turkish lira swap transaction volume in the London market was around 500 billion dollar monthly; after 2018, this figure went back to 350 – 400 billion dollars.

Table 1

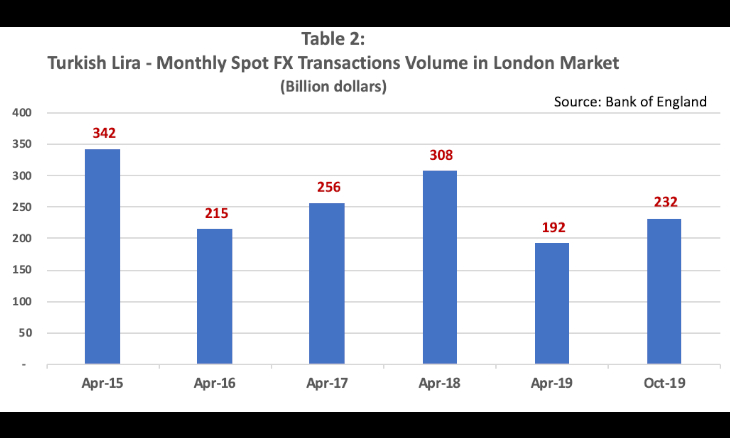

Turkish lira spot foreign currency transactions were around 250-300 billion dollars monthly, but they went back to 200 to 230 billion dollars.

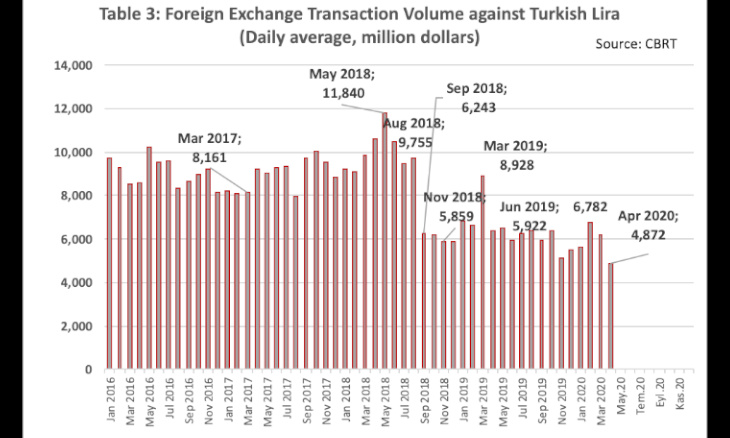

According to Central Bank data, the foreign exchange spot transactions volume of commercial banks in Turkey was at the daily average of 8 billion dollars before August 2018, however, this figure dropped to 4.6 billion dollars in April 2020.

The consequence of banning the Turkish lira to foreigners has been shallowing the markets where the value of the Turkish lira was originating and forming. Would a currency be fragile in a shallow market, or in a deep and high-volume market? We know the answer; the Turkish lira is more fragile now in the shallow market.

Let us come to the money transactions passing from payments system.

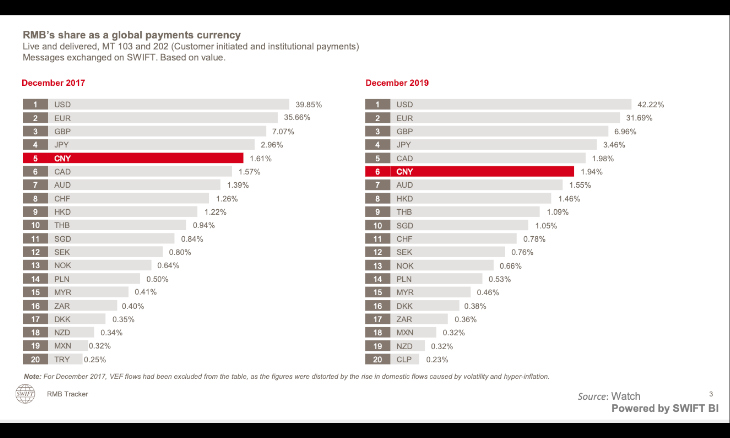

Swift system is a global money transfer system. It is quite a conservative institution in terms of publicity regarding data. From time to time, it issues a report based on the remnibi tracker system it has formed for the yuan. From there, there is an opportunity to find a clue for the lira. In the January 2020 tracking report, such a table emerges in global payments.

On top of the 2017 list, there is the U.S. dollar, with the 39.8 percent of all payments. The Turkish lira is at the 20th place on the list with 2.5 per mille (thousand) of all payments.

Two years later, at the end of 2019, the share of the Turkish lira has dropped and another currency has taken its place, the Chilean peso. Turkish lira is no longer on the top 20.

All that has happened points out to one phenomenon: The Turkish lira, unfortunately, is a currency the international validity and usage of which is highly wounded.

It has been 30 years when the foreign exchange regime introduced foreign currency freedom in 1989. The convertibility of the Turkish lira which was obtained very hardly and step by step has been inflicted major wounds in the past two years under bad management. This is a huge pity.