The forex vacuum in Ankara

Can the forex loss in Turkey be recovered without sending the bill to the public? If first signs of the establishment of political normalization, democratization and rule of law emerge in a powerful way in Turkey, then the “shrunken” foreign currencies will come back to the system.

On a flat land, underground water may be pumped to the surface by electric motors and used for agricultural irrigation while everything looks fine. One day, though, you may come across a sinkhole with a collapse of the earth’s surface. It is exactly this collapse that Ankara has been creating for the past two years in general in the economy and in particular in forex reserves.

When the signal flare of early elections was fired on April 17, 2018, the reserves of the Central Bank were 112 billion dollars. Out of this, 25.6 billion dollars were gold, 86.6 billion dollars were foreign currency reserves. Excess foreign exchange reserves exceed liabilities, in other words, foreign exchange position surplus was 32 billion dollars. When June 24 elections were held, reserves had gone back to 103 billion dollars.

After elections, the first cabinet of the “presidential government system” was formed on July 9, the seat in charge of economy management was given to the son-in-law of the President.

This was the threshold when economic politics in Turkey went into a crisis. Also, it was then when crisis management entered a bad lane never seen before.

It was in August 2018, when the diplomacy tactic that can be summarized as “Give me the imam and I will give you the pastor” that went parallel with the arrest of Pastor Andrew Brunson in İzmir, the Aegean port city. [Turkey thought the self-exiled Muslim preacher in the USA, Fetullah Gülen, accused of being behind the July 15, 2016 coup attempt, would be exchanged with Pastor Brunson.] Then came the US sanctions and a severe crisis was triggered. The economic crisis that has been expected to arrive any time since 2015 was prompted. The forex rates skyrocketed; the inflation erupted. A harsh interest rate boost curbed this, but the theme of “when the presidential system is enacted, then you will see how the interest rates will be kept down” was no longer applicable.

By the time Pastor Brunson went back to his country on Oct. 12, 2018 after a court freed him, foreign currency reserves had eroded to 88 billion dollars.

However, local elections scheduled for March 2019 were nearing and on one hand, the high interest rate, and on the other hand, the pressure of the forex rate were bothering Ankara just before the elections.

Within this framework, during the period between January 2019 and April 2019, public banks was started to intervene exchange rate through “back door” methods. These sales were done through brokers thus they did not attract much attention but one week before the local elections, this was understood when forex reserve erosion was noticed in the Central Bank balance sheet. This brought an additional forex rate leap. The effort to hold the forex rate stable had caused it to leap.

After this date, swap transactions were started. This was first to hide the erosion in the CB forex reserves and second to fill the gap caused by the erosion. But there was one problem: In the swap transactions which are based on a transaction that is done today and will be paid back at a future date, while the foreign currency entry is shown as an asset in the balance sheet, the liability of the future date to be paid was hidden outside the balance sheet. Each 1 billion dollar taken with swap was increasing the reserves, but they were not shown as a liability in the passive side of the balance sheet.

The dimension of forex erosion

While the sales in public banks were continuing, the size of the swap as of end of June 2020 reached 58.8 billion dollars. This meant that while CB declared its total reserve including gold within the balance sheet as 90.3 billion dollars, when this swap amount was deducted, a total of 31.5 billion dollar worth of reserve remained. In the past two years, just for the sake of the “political continuity,” the poor management in the economy has eroded a foreign currency reserve of 60 billion dollars.

This calculation does not include the potential foreign currency incomes the Central Bank has been deprived of. For example, in the two-year period between June 2018 and June 2020, the total of the foreign currency entries from returns of the rediscount loans the Central Bank lent to foreign currency earning companies was 41.5 billion dollars. Only due to this item, the forex reserves should have increased this much. This is not happening. Thus, the size of the foreign currency reserve eroded is more than 100 billion dollars.

When other on balance sheet foreign currency liabilities of the Central Bank are taken into consideration, the current foreign currency position is around 40 billion dollars negative. In other words, against 100 billion dollars’ worth of liabilities, the CB has 60 billion dollars. This means, in two years, we have gone from a surplus of 32 billion dollars to 40 billion dollars deficit.

Public banks, which eroded the foreign currency reserves of CB from the “back door” with political directive, have additionally also started eroding the foreign currencies in their own balance sheets. This has reached 10 billion dollars, as can be detected from Banking Regulation and Supervision Agency (BDDK) data. Thus, together with the Central Bank, all public banks have reached an open foreign currency position of roughly 50 billion dollars.

The problem is that much of “back door” interference and foreign currency circulations were not able to curb the forex rate. The reason for that is bad management and a deep distrust.

The thing that the inexperienced economy management in Ankara does not understand is that if you have not been able to achieve confidence and reputation politically, then you cannot protect the value of your own currency by selling currencies others have printed.

Reserves are over, now bring required reserves

First the reserves of the Central Bank then the reserves of public banks were eroded, while Ankara was freely spending all the ammunition. Then, they had private banks in their sights. A portion of the foreign currencies of these banks were already taken through the swap channel. An extra liability was imposed to these banks on July 18 by increasing foreign currency reserve requirements by 3 points.

In a statement, it was said that with this increase, some 9 billion dollars were expected to be deposited in the Central Bank. But it did not happen. Some banks decreased other assets being held at CB accounts and all together a net amount of 6 billion dollars were deposited.

While this step was taken, according to Bloomberg’s story, economy officials from Ankara called private banks and they were “recommending” that they acquire their foreign currency risks not from spot markets anymore but from futures markets. The meaning of this is following: “If your clients buy foreign currency from you, you should not enter the spot market and buy foreign currency to fill the deficit. Do forward transactions in BİST (Borsa Istanbul) and VİOP (derivatives exchange). Ankara, having finished all its ammunition, having seized the last foreign currencies left in the banks through required reserves, was recommending “forex transaction without foreign currency.”

Since there was no foreign currency left to interfere, it was recommended to the banks that instead they should do Turkish Lira-settled forward foreign exchange contracts (non-deliverable forward).

In other words, banks would buy futures from a certain forex rate terminal contracts (of course the CB would sell it), and when due, instead of buying forex they would take the difference at the forex rate from the other side. Separately, it was announced that the Central Bank also would be operating in this market.

Fine, but foreign currency, at some point will be required for those who need to transfer foreign money abroad and who will need to pay for imports. They will, of course, enter the market and buy.

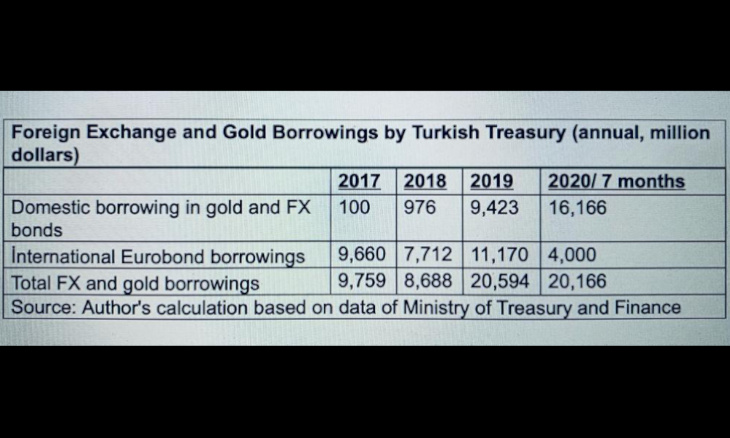

The forex appetite of the Treasury

From the second half of 2018, the new economy administration, formed with the presidential government system, has been “crushing” the reserves as such. On the other hand, they turned toward quite a lot of foreign currency and gold borrowings. With this, it was hoping to relatively lower the Turkish Lira borrowing, thus providing a fall in interest rates. Meanwhile, foreign currency and gold held by corporate investors (investor and pension funds), companies and individuals were targeted, regarded as a “source.” In fact, a significant portion of them were already in the system.

In the past, the Treasury would do its forex borrowings from abroad limited to principal payments. As a policy, foreign currency or gold exports were not preferred for citizens or corporate investors domestically. In 2018, this was disrupted with the new regime. As can be seen from the chart, domestic borrowing in gold and forex bonds have reached, in the first seven months of the year, 16 billion dollars.

While 2017, 2018 and 2019 annual principal and interest payments of foreign loans were 11.2, 11.1 and 10.7 billion dollars respectively; borrowings were 9.7, 8.6 and 20.5 billion dollars.

While the estimated foreign loan repayments in 2020 was 10.6 billion dollars, forex and gold borrowings done in the first seven months of the year have reached 20.1 billion dollars.

The forex vacuum in Ankara is absorbing all available foreign currency. Because of this, Ankara has eroded the foreign currency reserves of the Central Bank and public banks, lowered the reserves of private banks with an increase in reserve requirements. It is now absorbing the foreign currencies of other corporate investors and citizens through domestic borrowing.

Ankara is telling its citizens to “keep Turkish Liras,” telling other countries to trade with Turkish Lira, but it is borrowing foreign currency and gold, hence encouraging dollarization domestically.

This kind of free splurge period that has no political framework has not been seen in any term of any government. Even at its current state, an enormous forex wreckage has been created and, at the same time, it is, all by itself, an economic security issue.

Not the end of the world

The forex rate loss stemming from the 50 billion dollars open forex position is a potential public loss. Can this loss be recovered without sending the bill to the public? Even if the loss is not able to be recovered, if this political state of affairs does not go on for a long time, then its dimensions might be lessened.

If first signs of the establishment of political normalization, democratization and rule of law emerge in a powerful way in Turkey, then the “shrunken” foreign currencies will come back to the system.

With confidence building, it is possible to rapidly recover. On one hand, the residents may move away from foreign currency and enter into the system, and, on the other hand, non-residents may bring forex to the country and create demand for Turkish Lira.

Without the political crisis being solved, the economic crisis is not possible to be solved.

For this reason, there seems to be no other way than each “political neighborhood” in Turkey to engage in a joint restoration and normalization effort, possibly through protecting their own “neighborhood” features.